If you have spent any time reading about technology or finance in the past few years, you have almost certainly encountered both of these words — Bitcoin and blockchain. They appear together so frequently that many people assume they are the same thing, or that one is simply another word for the other.

They are not the same thing. Understanding the difference between them is one of the most useful pieces of financial and technological literacy you can have in 2025, because both concepts are becoming increasingly relevant to everyday life — from how money moves across borders to how legal contracts are executed to how digital ownership works.

This guide will explain both from scratch, clarify exactly how they relate to each other, and tell you why any of it matters to someone who is not a developer, an investor, or a technology professional.

Start Here: The Simple Version

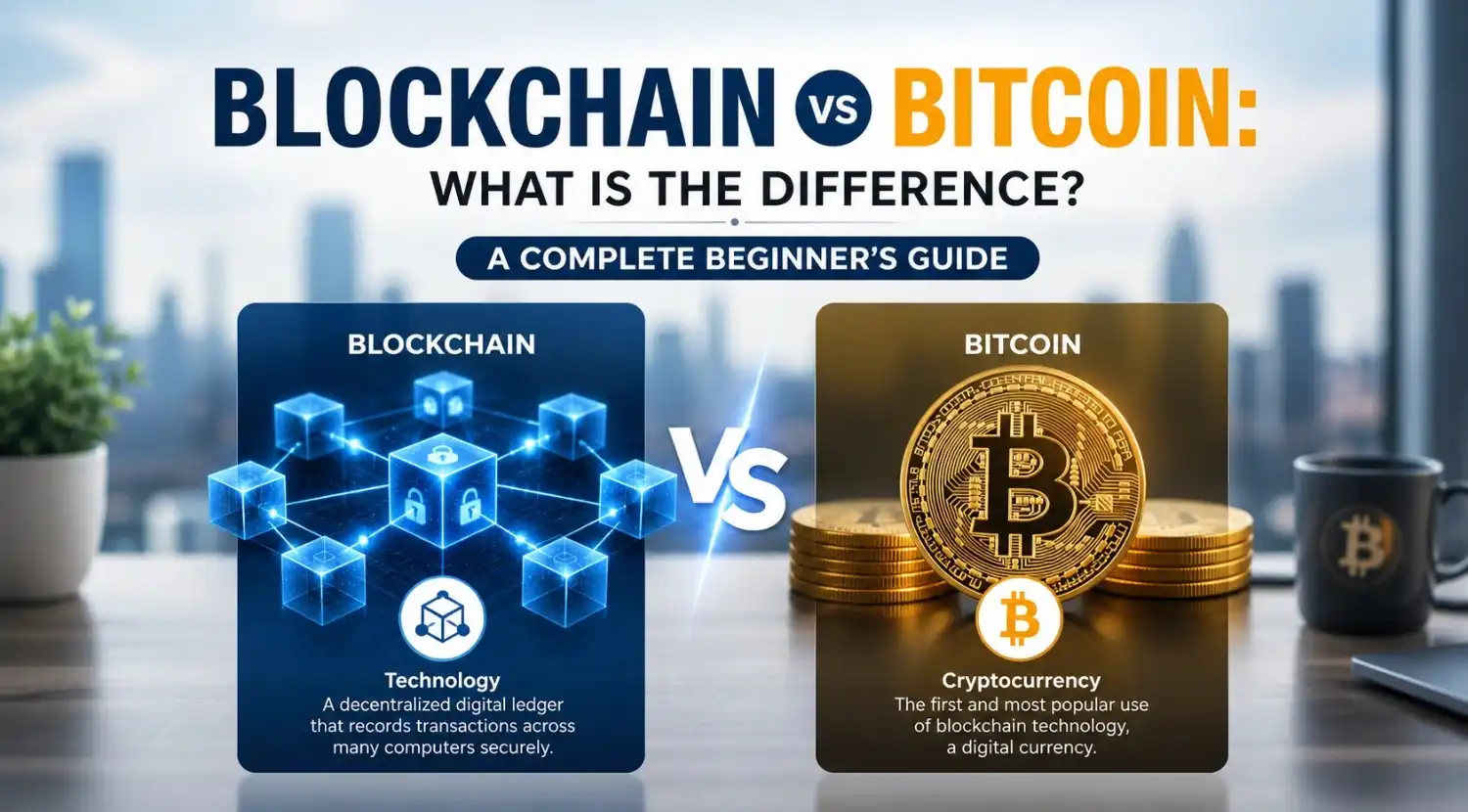

Here is the relationship between blockchain and Bitcoin in one sentence: Bitcoin is a currency that runs on a blockchain, but blockchain is a technology that can be used for thousands of things that have nothing to do with Bitcoin.

Think of it this way. The internet is a technology. Email is one application that runs on the internet. You would not say the internet and email are the same thing — the internet existed before email, and it supports countless other applications. The relationship between blockchain and Bitcoin is similar. Blockchain is the underlying technology. Bitcoin is one application built on top of it.

With that foundation in place, let us look at each one properly.

What Is Blockchain?

A blockchain is a specific type of database. To understand what makes it different from a regular database, it helps to understand how ordinary databases work.

When you use a banking app and check your account balance, that number is stored in a database controlled by your bank. The bank can read it, write to it, update it, and in theory alter it. You trust the bank to record the correct number and not tamper with it, and you trust regulators to hold the bank accountable if they do. The database is centralized — one institution controls it.

A blockchain is a decentralized database. Instead of being stored in one place and controlled by one entity, it is copied across thousands of computers simultaneously. Every participant in the network holds a complete copy of the entire database. When new information is added, it must be verified and agreed upon by the network before it is recorded — and once it is recorded, it is practically impossible to alter.

The name “blockchain” comes from its structure. Data is grouped into blocks. Each block contains a set of transactions or records, a timestamp, and a unique code called a hash. Critically, each block also contains the hash of the block before it. This links every block to the one that preceded it, creating a chain. If someone tried to alter a block in the middle of the chain, its hash would change, which would break its connection to every block that follows it — and the rest of the network would immediately reject the alteration.

This structure gives blockchain three properties that make it genuinely useful:

Transparency. Every transaction recorded on a public blockchain is visible to anyone who wants to look. There is no hidden ledger, no privileged access.

Immutability. Once data is recorded, it cannot be changed or deleted without the consensus of the entire network — which in practice means it cannot be changed at all.

Decentralization. No single person, company, or government controls the database. It is maintained collectively by everyone who participates in the network.

These properties have implications far beyond cryptocurrency. Any situation where multiple parties need to share a trustworthy record — without needing to trust each other or a central authority — is a potential use case for blockchain.

What Is Bitcoin?

Bitcoin is a digital currency — the world’s first decentralized cryptocurrency. It was created in 2008 by an anonymous person or group using the pseudonym Satoshi Nakamoto, who published a document called the Bitcoin whitepaper describing a system for electronic cash that could be sent from one person to another without going through a bank or any other financial institution.

Bitcoin was the first real-world application of blockchain technology. Every Bitcoin transaction ever made — every time someone has sent or received Bitcoin since its creation — is recorded on the Bitcoin blockchain, a public ledger that anyone can view and verify.

Here is how a basic Bitcoin transaction works. Suppose you want to send Bitcoin to a friend. You initiate the transaction from your digital wallet. That transaction is broadcast to the Bitcoin network, where thousands of computers — called nodes — verify that you actually have the Bitcoin you are claiming to send and that you have not already spent it elsewhere. Once verified, the transaction is grouped with others into a block, that block is added to the chain, and your friend receives the Bitcoin. No bank processed the transaction. No government issued the currency. No central authority verified the exchange.

Bitcoin has a fixed maximum supply of 21 million coins, written into its code from the beginning. This scarcity is deliberate and is one of the reasons many people treat Bitcoin as a store of value comparable to gold — something whose value is partly derived from the fact that there will never be more of it beyond a defined limit.

New Bitcoin is created through a process called mining, in which powerful computers compete to solve complex mathematical puzzles. The winner adds the next block to the blockchain and is rewarded with newly created Bitcoin. This process also serves the function of securing and verifying the network.

The Key Differences, Clearly Laid Out

Now that both concepts are defined, here is a direct comparison across the dimensions that matter most.

Nature. Blockchain is a technology — a method of storing and verifying data. Bitcoin is a currency — a medium of exchange and store of value.

Scope. Blockchain can be used for an essentially unlimited range of applications: supply chain management, healthcare records, voting systems, real estate transactions, legal contracts, digital identity, and much more. Bitcoin has one primary function: to serve as a decentralized digital currency.

Dependency. Bitcoin cannot exist without blockchain — it requires the blockchain to record and verify every transaction. But blockchain can exist without Bitcoin — and does, in countless applications that have nothing to do with cryptocurrency.

Ownership and control. The Bitcoin blockchain is public and permissionless — anyone can participate. Other blockchains can be private or permissioned, meaning access is restricted to approved participants. A hospital system might use a private blockchain to share patient records securely among authorized providers, with no connection to cryptocurrency at all.

Volatility. Bitcoin’s value fluctuates significantly based on market forces, sentiment, regulation, and adoption. Blockchain as a technology does not have a price — it is infrastructure.

What Else Can Blockchain Do?

This is where the technology becomes particularly interesting for people who have no interest in cryptocurrency whatsoever.

Supply chain and logistics. Blockchain allows every step of a product’s journey — from raw material to factory to retailer to consumer — to be recorded on an immutable ledger. Walmart uses blockchain to trace food products, allowing contamination sources to be identified in seconds rather than days. Luxury goods companies use it to verify authenticity and combat counterfeiting.

Healthcare. Patient records stored on a blockchain can be accessed by any authorized provider while remaining completely secure from unauthorized alteration. Clinical trial data recorded on a blockchain cannot be manipulated after the fact, increasing the integrity of medical research.

Real estate. Property transactions involve enormous amounts of paperwork, multiple intermediaries, and significant potential for fraud. Blockchain-based land registries can make property ownership verifiable, transferable, and tamper-proof — a particularly significant development for countries with historically unreliable land record systems.

Digital identity. A blockchain-based identity system allows individuals to control their own verified credentials — passport details, educational qualifications, professional licenses — without relying on any single institution to store and validate them.

Smart contracts. These are self-executing contracts written directly into blockchain code. When pre-defined conditions are met, the contract executes automatically — no lawyer, no notary, no bank required. An insurance policy could automatically pay out when flight delay data confirms your flight was late. A property sale could transfer ownership the moment payment is confirmed.

Common Misconceptions Worth Clearing Up

Misconception: Blockchain and cryptocurrency are the same thing. They are not. Cryptocurrency is one application of blockchain technology. Blockchain is the underlying infrastructure that can support thousands of different applications.

Misconception: Bitcoin transactions are anonymous. They are pseudonymous, not anonymous. Every transaction is publicly recorded on the blockchain. While the names of the parties are not displayed, wallet addresses are visible — and with enough analysis, transactions can often be traced back to real identities.

Misconception: Blockchain is completely unhackable. The blockchain itself is extremely difficult to alter. But the applications built on top of it — exchanges, wallets, smart contracts — have been hacked. The technology is robust; the human and software layers around it are not always so.

Misconception: Blockchain requires cryptocurrency to work. Private and permissioned blockchains used by corporations and governments operate entirely without cryptocurrency. The blockchain mechanism — distributed ledger, cryptographic verification, immutable record — functions independently of any token or coin.

Why Does Any of This Matter to You?

Even if you never buy Bitcoin and never interact with a blockchain application directly, this technology is already reshaping systems that affect your life.

The financial system is being rebuilt around it. Central banks in dozens of countries are developing Central Bank Digital Currencies — government-issued digital money that uses blockchain infrastructure. Cross-border remittances that currently take days and charge high fees are moving to blockchain rails. The way money moves is changing.

The way ownership works is changing. Digital ownership of assets — art, real estate, intellectual property, credentials — is increasingly being recorded on blockchains. The concept of truly owning something digital, in a way that is verifiable and transferable, is new and consequential.

The way trust works is changing. For centuries, trust in transactions has been mediated by institutions — banks, governments, courts, notaries. Blockchain offers a technological alternative: trust enforced by mathematics and distributed consensus rather than by any human authority. Whether that is better in every case is debatable. That it is different and significant is not.

Conclusion

Blockchain and Bitcoin are related but distinct. Bitcoin is a revolutionary application of blockchain technology — the first proof that a trustworthy financial system could exist without central control. Blockchain is the broader infrastructure that makes Bitcoin possible and that is now being applied to problems ranging from food safety to healthcare to property rights.

Understanding the difference does not require you to invest in cryptocurrency or learn to write code. It requires only that you recognize the nature of what is being built — a new kind of record-keeping infrastructure that removes the need for trusted intermediaries in an enormous range of human transactions.

That shift is already underway. Knowing what it is puts you in a better position to navigate it.